Discover the power of negative gearing.

With the high costs of living, high taxes and high property prices in Australia, it’s almost impossible to build up enough wealth.

Superannuation can help, but unless you make huge contributions over a very long time, it won’t go too far. The problem has only gotten worse with the 2017 super reforms, which have seriously reduced the amount of money you can contribute to super.

That’s where negative gearing can help you.

Negative gearing is a powerful tool that’s helped the rich get richer, and everyday Australians gain substantial wealth. While there are definitely pros and cons to negative gearing, we believe that the positives hugely outweigh the negatives. And if it’s done correctly, it’s not hard to significantly reduce the risks.

This e-book’s been written to help give you a better understanding of gearing and how it works- and it’s a lot easier to understand than most people realise.

Negative gearing is about a lot more than your investment income being below your investment expenses.

The long-term results can be life-changing.

Tax Effective Accountants has helped clients achieved amazing results from negative gearing.

And hopefully after you’ve read this entire e-book, you’ll think about making an appointment to talk to a qualified tax accountant or financial planner that can help you customise a geared investment plan to help you secure your financial future.

If you’d like to see one of our specialised wealth accountants, book your free financial health diagnostic, valued at $395, and discover how negative gearing can help you achieve financial freedom today.

Speak to a wealth accountant todayMake an appointment >Request a callback >

Disclaimer

This e-book has been written by Tax Effective Accountants.

This e-book does not take into account your financial situation or personal circumstances. All the information you are about to read is general in nature and should not be used as a substitute for financial advice.

Please make sure you get professional advice prior to implementing a gearing strategy.

Contents

- Discover the power of negative gearing

- Disclaimer

- Contents

- What is gearing?

- What is negative gearing?

- What assets can you negatively gear?

- Types of gearing facilities

- The business end of negative gearing

- How to negatively gear residential property

- Client case study 1: negatively gearing residential property

- Reducing investment costs with depreciation

- Client case study 2: using depreciation to reduce investment costs

- Negatively gearing a share portfolio

- Client case study 3: negatively gearing a share portfolio

- Increase cash flow with a withholding tax variation

- Borrowing money through super

- Advantages of negative gearing

- Disadvantages of negative gearing

- How to minimise the risks of negative gearing

- Who is negative gearing suited for?

- The best time to act

- Advanced negative gearing strategies

- Where to from here?

- Book an appointment

Gearing- what is it?

Before getting into negative gearing, it’s important to understand gearing in general. So, let’s take a step back and quickly take a look at what gearing is.

Gearing just means borrowing money to invest.

It can accelerate your potential to grow your wealth because it provides you with more money to buy larger investment assets that you couldn’t have purchased otherwise.

As long as your investment achieves a capital gain, or goes up in value, and provides an income that's greater than the costs of borrowing, gearing can really magnify your gains. But, if your investment were to achieve a capital loss, or go down in value, that loss could be significant too.

Simple example of how gearing works

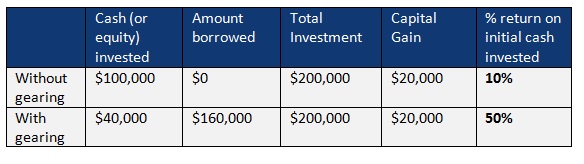

John wants to put $200,000 into an investment. He has $200,000 in savings.

Let’s look at a couple of scenarios- one where John uses all of his money to invest, and another where he uses only $40,000 of his money and borrows $160,000.

Let’s assume that the $200,000 investment makes a $20,000 (10%) gain.

As you can see, gearing gets you a return that’s 40% higher on the exact same investment.

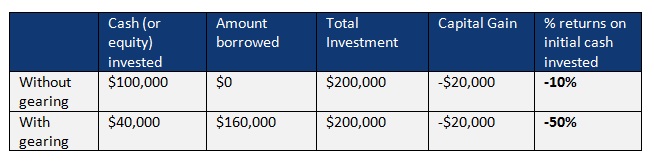

Now let’s look at the flip side. What if the investment went down by $20,000?

Looking at the above examples, you can see how gearing can accelerate the pace your investments go up and go down.

However, you should keep in mind that all good long-term investments go up in value over time regardless of any short-term market fluctuations.

What is negative gearing?

Negative gearing occurs when the interest you have to pay on the money you borrowed plus all other investment costs is greater than the income you’re making from the investment.

This means the investor has to have surplus income or savings to meet the shortfall.

This shortfall, the difference between your investment expenses and income, can be claimed as a tax deduction. This reduces the amount of tax you pay and gets you a tax refund at your marginal tax rate, which effectively reduces the cost of your investment.

Simple example of how negative gearing works

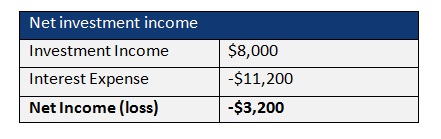

If we look at the previous example where John puts $200,000 into an investment, he contributes $40,000 and borrows $160,000.

Let’s assume that John earns an investment income of $8,000 and his investment loan interest rate is 7%.

We’ll also assume that there are no other ongoing investment costs.

John earns $100,000 and has a marginal tax rate of 39% including the Medicare Levy.

This is how it works:

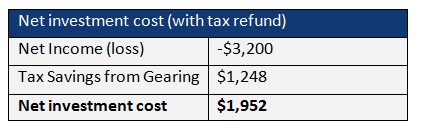

This table shows that John makes a loss of $3,200 each year.

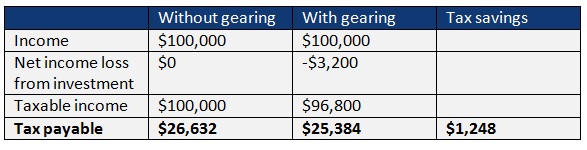

John’s able to add this negative amount to his taxable income- so he’ll be taxed on $3,200 less.

To illustrate:

This means that gearing has reduced John’s tax liability by $1,248. Hence, the after-tax loss is reduced from $3,200 to $1,952.

How John can make money through gearing

As long as John’s $200,000 investment grows by more than $1,952, or 0.976% each year, he’ll create wealth from his investment.

It’s highly unlikely for any solid long-term investment to grow by less than 1% a year.

So, John’s chances of making money on his investment are very high.

What assets can you negatively gear?

When someone says “negative gearing,” property investments come to mind for most people. But negative gearing, as we now know, can refer to any situation where the investment costs are lower than the income the investment generates.

You can experience negative gearing on any asset, including:

- Residential property

- Commercial property

- Australian shares

- International shares

- Property trusts

- Businesses

As long as the investment generates taxable income, then the interest and other ongoing investment costs should be tax-deductible- you won’t need to pay tax on them.

Regardless of what the investment is.

But it’s not suitable for everything. Keep in mind that it can make very little sense to use gearing to invest in assets that provide no or very little capital growth, such as fixed interest or cash types of investments like term deposits and cash management trusts.

Types of gearing facilities

There are a number of different ways that you can borrow money to purchase investments.

1. Home equity loans

The most straightforward and cost-effective way to borrow money to invest is to borrow against the equity in residential property you own.

This just means that you use your home equity as collateral, or to secure the loan. Home equity refers to the value of your ownership in the property- or the value of the property minus your mortgage and any other costs you have to pay off.

The benefits of using home equity are:

- Cheaper interest rates than most other loans

- No margin calls where the banks can ask you to put in more capital if the value of your property goes down

- You don’t have to contribute any of your own funds to the investment- you can borrow the entire purchase price, plus costs

- Home equity loans also include line of credit loans, which are commonly used by investors.

Here’s how it works.

Example: Buying property using home equity

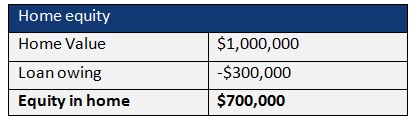

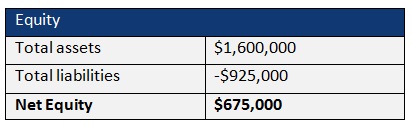

Hamish is an IT consultant earning an income of $150,000 per year. He has a home valued at $1,000,000 with a loan owing of $300,000. This means that Hamish has $700,000 in home equity.

Hamish wants to purchase an investment property for $600,000. He doesn’t have the $600,000 plus costs he needs to buy the property.

He decides to take out a home equity loan. He provides his home as security, as well as the investment property, and borrows the entire purchase price plus costs – approximately $25,000, including stamp duty and legal fees from the bank.

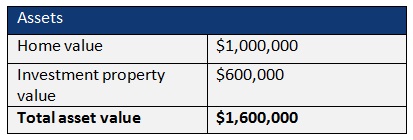

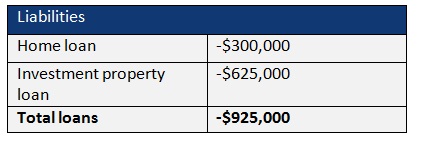

This is what Hamish’s new asset position looks like:

Hamish's assets:

Hamish's liabilities:

Hamish's equity:

As you can see, Hamish’s equity has dropped by $25,000, the cost of stamp duty and legal fees. However, he still holds $675,000 of the original $700,000.

The new loan of $625,000 is what makes up the “gearing” part of negative gearing.

If the value of the property reduces, the banks do not require you to make any extra contributions like they do with margin loans- which we’ll discuss below.

Your only obligation is to meet your loan repayments.

2. Margin loans

Another way to fund investments is through a margin loan facility. With a margin loan, you’re required to contribute your own equity to be used as security for the borrowing.

The main types of equity include existing cash, shares, managed funds or exchange traded funds.

The lending institution will loan you a portion of the existing value of the equity you choose to offer, usually between 40% and 80%.

If the margin loan outstanding later goes above the lender’s permitted loan to value ratio as a result of a decrease in the value of the asset, the lender will make a margin call.

If a margin call is made, you’ll have to either make a cash contribution or sell some of the assets the lender is holding as security to bring your loan back within the lender’s acceptable limit.

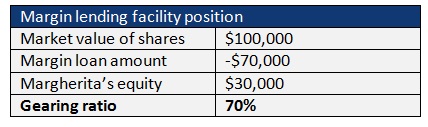

Example: Borrowing to buy shares using a margin loan

Margherita wants to invest money to buy $100,000 in some blue-chip shares. She only has $30,000 in cash, so she wants to use a margin loan to help her reach her investment goal.

Margherita goes to a lender that offers a loan to value ratio of 70% on the shares she would like to purchase.

Therefore, Margherita contributes her $30,000 (30%) in cash and borrows $70,000 (70%) from the lender to purchase her $100,000 share portfolio.

Margherita’s margin lending facility position can be summarised as follows:

Note that margin lenders often allow a buffer so that small market fluctuations don’t result in a margin call. The buffer can be between 5 to 10% of the maximum loan to value ratio the lender will provide you.

This means, for example, that if the value of the shares dropped below $90,000 (a 10% drop), Margherita could be in breach of her margin limit, in which case she’d have 24 hours to correct the situation.

Unless a margin call is made, you’re not obliged to take any action to restore your loan to value ratio position.

You can minimise the risk of a margin call by borrowing more conservatively.

For example, if Margherita made an initial contribution of $30,000 and borrowed only $30,000 to purchase an asset, her share portfolio would have to drop by over 33% in order for a margin call to arise.

Speak to a wealth accountant todayMake an appointment >Request a callback >

The business end of negative gearing

The power of negative gearing

Now that you have an idea of what negative gearing is, let’s look not only at how it works, but also how you can use it to create significant wealth over the long-term.

We’ll illustrate 3 different examples for you.

If your financial situation allows for it, you could very well implement all 3 scenarios at the same time.

Please seek financial advice before proceeding with any gearing strategy.

How to negatively gear residential property

When looking at gearing into property, it’s important that you understand what ongoing property costs include.

Ongoing property investment costs include:

- Interest payable on investment loans

- Body corporate fees (if you purchase a strata title property including a unit or townhouse)

- Real estate agent fees

- Council and water rates

- Insurance

- Repairs and maintenance costs

- Traveling expenses to and from your property

- Ongoing bank fees

- Any other ongoing expenses incurred

Only ongoing costs can be claimed against your rental income- that is, you can only claim a tax deduction on ongoing costs. Any capital expenses or one-off costs for improvement to your property (renovations) cannot be claimed if the cost is greater than $300.

One-off costs can, however, be depreciated and claimed as non-cash expenses over a number of years. For example, if you replaced the carpet and it cost you $5,000, you wouldn’t be able to claim the entire amount as an expense.

However, you may be able to claim 20% of the cost, or $1,000 in the first year, then another 20% of the remaining $4,000 ($800) in the second year, 20% off the remaining $3,200 in the third year and so on.

So, let's look at an example of how negative gearing works with property.

Case study 1

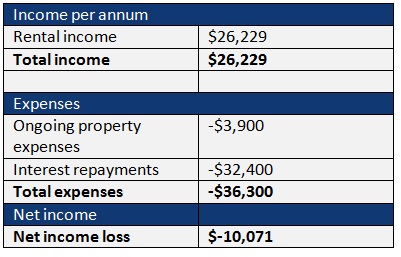

Adam is a digital marketing specialist and earns $120,000 per annum. He’s saved $110,000 over the years and wants to invest his money tax effectively.

He prefers to invest in the property market. He finds a property valued at $600,000 and intends to rent it out for $520 per week.

He puts in a 10% deposit plus costs including stamp duty, loan mortgage insurance and legal fees totalling $95,000, and borrows $540,000 from the bank.

The current interest rate on his loan is 6%. This equates to $32,400 in interest repayments each year.

Adam appoints a property manager who pays all his property expenses. These costs come to $3,900 per annum.

There’s also a 3% vacancy rate.

How do the numbers actually look?

Net property cash flow

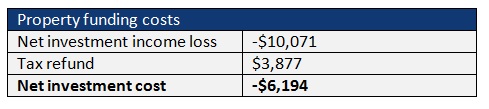

These figures show that Adam makes a loss of $10,071 each year.

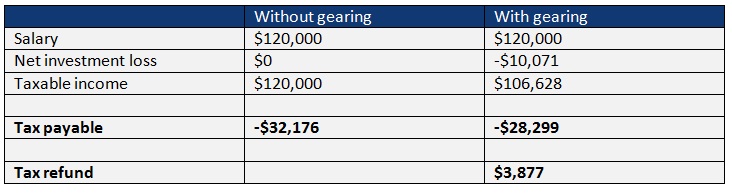

Adam is able to add this negative amount to his assessable income, reducing his taxable income and providing him with a tax refund. This will bring down his net loss and the ongoing costs of his investment property.

Calculation of tax refund

This table shows us that negative gearing has reduced Adam’s tax liability by $3,877.

This means that his net loss of $10,071 will fall by his tax refund of $3,877, bringing down the total cost to fund his $600,000 property to $6,194 per annum.

What return does Adam’s $600,000 investment property need to make a profit?

For Adam to create wealth through his investment, the property would have to grow by more than 1.03%.

For this type of long-term investment, it’s extremely likely that it will grow by far more.

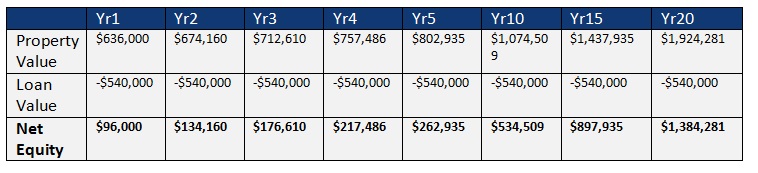

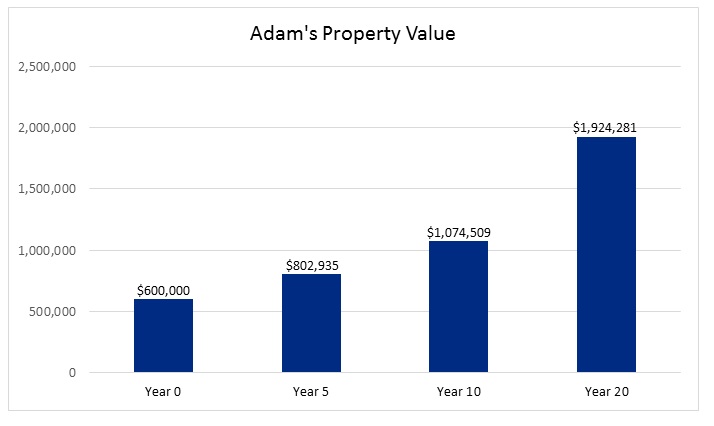

Growth of investments over 20 years

Let’s assume that there’s a 6% property growth rate and that you pay interest only on your loan facility to simplify the scenario.

That is a $1,384,281 net capital gain over 20 years.

Versus an expense of only $6,194 per annum.

What have we learned about negative gearing?

As you can see from this case study, the costs of funding a geared investment property can be quite minimal, while the capital gains you can achieve can be incredibly high.

Remember- a negatively geared investment property will turn into a positively geared property which will earn rental income that’s higher than your expenses.

Speak to a wealth accountant todayMake an appointment >Request a callback >

How depreciation can significantly reduce the cost of investment

Did you know that as a property investor, you could be entitled to large tax deductions that can significantly reduce the ongoing costs of property investing?

Just like wear and tear on a motor vehicle or computer purchased for work purposes, the Australian Taxation Office will allow you to claim a tax deduction on the depreciation of your investment property against your assessable income.

Professional property investors know all about this.

As a matter of fact, a large number of them will take depreciation into consideration before purchasing an investment property.

Property investors can claim depreciation in two ways:

1. Depreciation on the capital works

The capital works allowance is a tax deduction that’s available for the structural component of a building.

More straightforwardly, it’s a deduction you can claim on the initial building costs of your property plus any structural improvements that may have been made.

Depending on the age of the building, you should be able to claim a 2.5% tax deduction off the original cost of the building or structural improvements for 40 years after acquiring it. If the building’s over 40 years of age, you will not be able to claim any deduction.

So, if you purchased a new property and the cost to build the structure of the property was $200,000, you could be entitled to a $5,000 tax deduction every year for 40 years.

Your tax deduction will be lower if the property’s older. The older the building, the fewer the number of years until the 40-year time period is over. In addition, the building costs you’ll be claiming your deduction against will most likely be lower.

So, if you purchased a property that’s 10 years old, the original building cost could have been $90,000. That would mean that you may only be entitled to a tax deduction of $2,250 (2.5% of $90,000).

2. Depreciation on fixtures and fittings

Fixtures and fittings can also be depreciated. These are essentially the assets within your property that have a limited lifespan.

The “lifespan” of each type of fixture and fitting is set by the Australian Taxation Office and the depreciation rate is calculated accordingly.

- Hot water service

- Ceiling fans

- Dishwashers

- Carpet

- Exhaust fans

- Washing machines

- Range hoods

- Smoke alarms

- Air conditioner

- Blinds and curtains

- Cooktops

- Security systems

- Ovens

- And more

Fixtures and fittings depreciate at a quicker rate than building or structural costs. Depreciation on the building is calculated on a prime cost basis- which just means the amount by which the asset falls in value is the same every year.

Fixtures and fittings depreciate a lot quicker because they generally use the diminishing cost method. That is, you’re able to claim higher amounts initially, with these amounts gradually going down each year based on the previous year’s value less what was claimed that year.

Changes to depreciation - what you need to know

To try to reduce pressure on housing affordability, the government will limit depreciation deductions on fixtures and fittings- they’ll now only apply to actual expenses you’ve incurred as the investor.

So, unless you yourself have physically purchased the items, you cannot depreciate them.

This measure is intended to stop investors from claiming depreciation on assets they didn’t purchase, and save the government over $260 million a year.

The good news is that any property purchased or exchanged prior to May 9th 2017 isn’t affected. Also, the measure only applies to residential property investments, not commercial, industrial or other non-residential ones.

This raises questions about brand new investment properties and who’s actually considered to have acquired the assets.

We believe that when the legislation is finalised, you’ll still be able to claim depreciation on the fixtures and fittings, making brand new properties a very attractive property investment option.

Note that nothing has changed with regards to claiming depreciation on the building costs. This will continue to apply regardless of whether you purchased a property prior to or after May 9th 2017.

Depreciation - brand new property vs older property

The newer the property, the more tax depreciation can be claimed.

A typical brand new two-bedroom unit, for example, can provide between $12,000 and $15,000 in tax deductions in the first year.

If you claim this at the highest marginal rate of tax, it can result in an additional tax saving and property cost reduction of between $5,640 and $7,040.

A brand new house, townhouse or duplex should provide an even larger tax depreciation allowance.

An old property may achieve only a few hundred dollars in tax refunds.

It all depends on the age of the property.

How depreciation can significantly reduce the ongoing property costs:

Case study 2

Let’s say that Adam from the example above instead decided to purchase a new three-bedroom unit for $650,000. He intends to rent out the property for $600 per week.

He borrows 90% of the purchase price ($585,000) and the bank charges him an interest rate of 6%, which equates to $35,100 per annum.

The ongoing property costs outside of his interest repayments are $6,200 per annum.

Because the property is new, Adam orders a depreciation schedule from an approved Quantity Surveyor who determines that he will be entitled to $13,000 in depreciation allowances in the first year.

We will also assume a 3% vacancy rate.

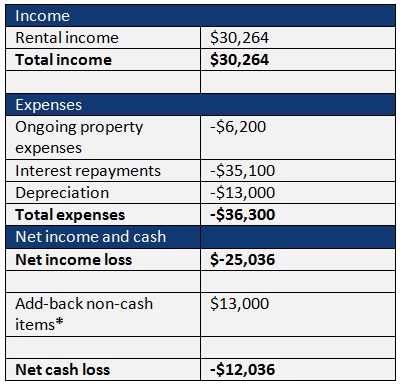

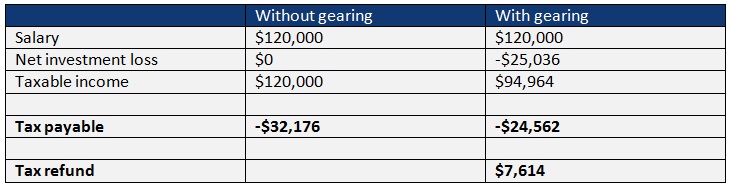

How do the numbers look when you include depreciation?

Net property cash flow

* Non-cash items are depreciation allowance

A little confused about why we added back the depreciation?

Here’s why.

Depreciation is not an expense that you pay for out of your pocket. It’s a deductible allowance that ‘brings up’ your net loss so that you can actually increase your tax deductions.

As a result of the depreciation expense, Adam is considered to have made a loss of $25,036 per year.

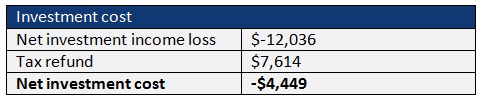

Once we’ve determined how much you can claim against your income, we add this amount ($13,000) back to give you your real out of pocket cost.

Calculation of tax refund

This table illustrates that negative gearing has reduced Adam’s tax liability by $7,614.

This means that his net investment property loss of $12,036 will reduce by Adam’s tax refund of $7,614.

Bringing down the total cost to fund his $650,000 property to $4,449 per annum.

What return does Adam’s $650,000 investment property need to earn to make a profit?

In order for Adam to create wealth, his property will have to grow by more than 0.68%. Any capital growth above this will be a profit.

The investment will almost definitely grow in value by far more than 0.68% over Adam’s investment horizon.

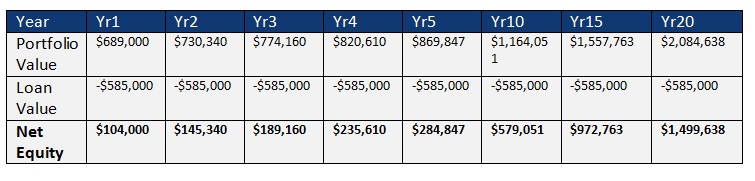

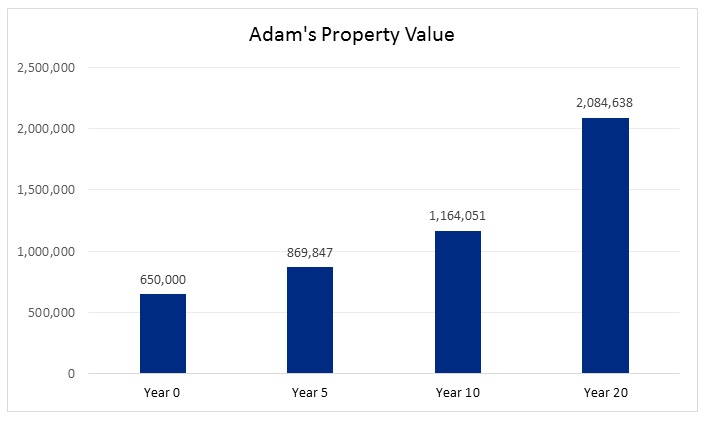

Growth of investments over 20 years

Let’s assume a 6% property growth rate

In 20 years, Adam could create an additional $1,759,498 in net wealth. This is something that would be almost impossible to achieve by saving alone.

What have we learned?

As you can see from this illustration, depreciation allowances can significantly reduce the ongoing investment costs of buying and holding an investment property, making it cheaper to hold a new, higher-priced property than an older property with a cheaper purchase price and lower loan value

Speak to a wealth accountant todayMake an appointment >Request a callback >

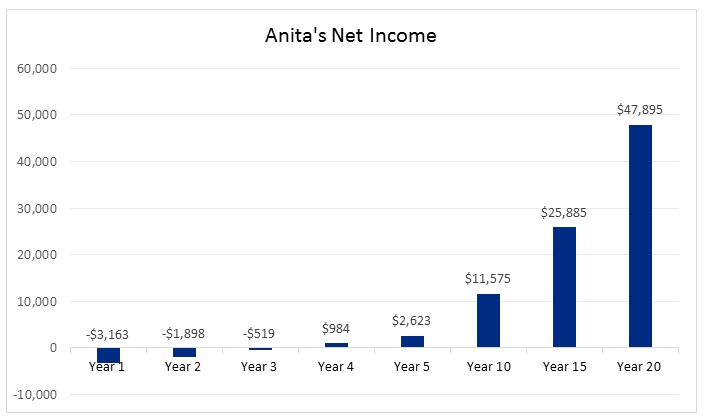

How to negatively gear a share portfolio

Case study 3

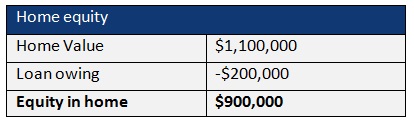

Anita is a business analyst earning $140,000. She has a home valued at $1,100,000 with a remaining home loan of $200,000. This mean she has equity in her home of $900,000.

Anita decides to use the equity in her home to purchase a $400,000 Australian share portfolio. Anita takes out a line of credit loan to make the purchase.

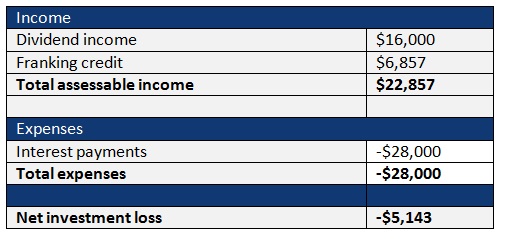

Her share portfolio pays her a 4% fully franked dividend.

Net investment cash flow:

This investment will make Anita an annual loss of $5,143, which will be included in and claimed as a tax deduction on her assessable income.

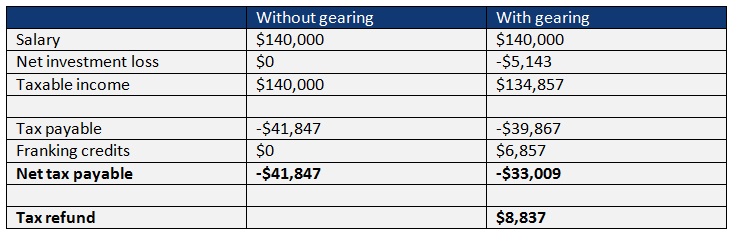

Calculation of tax refund from negative gearing

Once the tax loss has been claimed, Anita will receive a tax refund of $8,837.

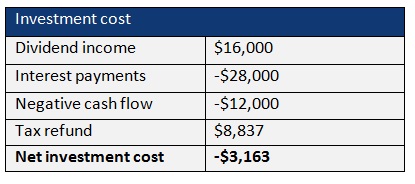

Calculation of net investment cost after receiving tax refund from negative gearing:

Now that we have the tax refund of $8,837, we find that the net investment cost will reduce to $3,163.

What return does Anita’s $400,000 investment need to earn to make a profit?

In order for Anita to create wealth, her initial $400,000 investment will have to grow by more than 0.79%. Any capital growth above this will create a profit for Anita.

Again, it’s extremely unlikely for such an investment not to grow far beyond this amount. Anita will very likely make a huge profit from this investment over the long-term.

Let’s assume a capital growth rate of 5% and that dividends are reinvested. We will also assume that Anita only pays interest on her loans.

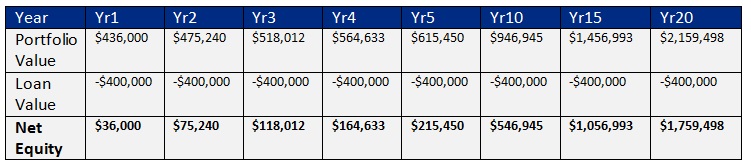

Net cost over 20 years

By reinvesting the dividends back into her portfolio, Anita’s $400,000 investment should become positively geared in year 4. This means that her portfolio dividends should exceed her interest repayments.

And in year 20, it should pay her an income stream of $47,895.

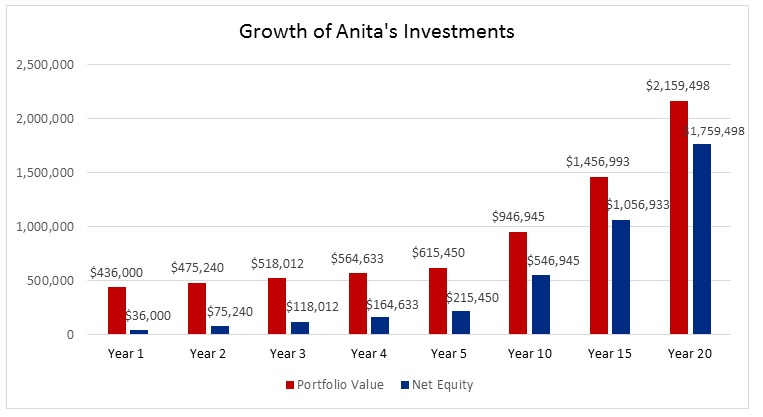

Growth of investments over 20 years

In 20 years, Anita could create an additional $1,759,498 in net wealth. This is something that would be almost impossible to achieve by saving alone.

From the above case study, you can see that gearing can be a very powerful wealth creation tool. With a combination of investments, time and compound growth, Anita should achieve substantial growth.

The longer the time frame, the greater the net return- so if you have a longer investment horizon and you’re looking to significantly boost your wealth over time, gearing’s definitely a strategy you should consider.

Speak to a wealth accountant todayMake an appointment >Request a callback >

Using a withholding tax variation to increase cash flow

When negative gearing, most investors rely on the tax refunds available to them to reduce the cost of their investment. But with most deductions, we wait until the end of the financial year before we submit our tax returns and wait for our tax refunds.

This can cause cash flow issues for investors whose surplus savings may not be large enough to pay the expenses upfront.

To avoid these cash flow issues, you can apply for a PAYG Withholding Tax Variation.

A PAYG Withholding Variation lets you receive your tax breaks each time you’re paid, so that you don’t have to wait until you lodge your income tax return after the end of the financial year.

Once your PAYG Variation is approved, the Australian Tax Office tells your employer to withhold less tax and effectively increase your pay by adding your tax savings to your income.

You can apply for your Variation yourself, but we recommend going to your accountant to help you so that you can get it done smoothly, and avoid any errors.

If your accountant hasn’t lodged a Variation on your behalf for existing properties that you own, then you may consider getting an accountant who would.

Did you know that you can borrow money through super?

Legislation allows self-managed super funds to borrow money to buy residential property, commercial property and shares, provided that certain conditions are met.

In addition to the wealth creation benefits we went through earlier, implementing a negative gearing strategy within a self-managed super fund allows your assets to benefit from being invested in a very low-tax environment where taxes on investment income are capped at 15% as opposed to your marginal tax rate of up to 49%.

Also, capital gains, if you’ve held the investment for more than 12 months, will pay no more than 10% tax on the gain.

Advantages of gearing investments in an SMSF

- You have to put in a larger deposit from your SMSF savings, which means your fund borrows less. As a result, investments tend to be close to self-funding

- You can save tens, if not hundreds of thousands of dollars in taxes thanks to the concessionally taxed environment SMSFs enjoy. For most Australians, SMSFs pay between 52.4% and 69.4% less tax on investments, which means the SMSF will keep considerably more of the investment returns when compared to buying a property in your personal name

- Your rental income, dividend income and super contributions should be more than enough to comfortably pay for any negative gearing shortfalls that might come up due to increased interest rates, loss of tenants or loss of income, making it a lot less risky of a proposition

- The loans in super are limited in recourse which means that if your SMSF can’t meet its loan repayment obligations, the banks have no recourse on any of your other super assets- only the property or investment that the SMSF loan has been used to purchase.

For more information about borrowing money to buy property through super, check out this e-book and learn more about SMSF property investing.

If you have a super balance of over $200,000 or combined balance of $200,000 with three other family members, this e-book is a must read.

Access your free guide today to find out how you can easily buy property through an SMSF.

Read now >

Advantages of negative gearing

There are many advantages to negative gearing, including:

- Gearing allows you to borrow more money so you can significantly increase the size of your investment portfolio

- The more money you have invested and earning compound growth over time, the greater the wealth you build in the mid to long term

- The ongoing investment costs are 100% tax deductible, which means you can receive large tax refunds that can significantly cut down your ongoing net costs

- The more equity and cash flow you have available for investment, the more you can gear to invest

- Most negatively geared investments eventually become positively geared investments, which means the investment income you earn will be greater than your ongoing investment expenses- this surplus cash can then be used to fund additional geared investment or to reduce debts

Disadvantages of negative gearing

There are also risks that you need to consider when negative gearing. They include:

- A fall in investment value can magnify your losses- which is why you need to take a long-term view so that you can give your investment time to recover any losses

- Negative gearing means that your investment is making a cash loss. The cash loss has to be paid out of your pocket

- If interest rates rise or if your investment pays you less income than anticipated then your loss will be increased and can impact your cash flow

- If you lose your income, you will still be obliged to pay your investment loan repayment and investment expenses

How to minimise the risks of negative gearing

Though gearing does have its risks, that are ways that you can considerably minimise them, which we summarise below

- Don’t over-commit. Only borrow as much money as you can comfortably afford to repay. Do the numbers and ensure that you can absorb a 2-3% interest rate hike without coming under financial stress. Understand that there will be times that your investment may not pay you an income due to short-term tenancy vacancies, interest rate rises, or you temporarily losing your job.

- Set up a cash reserve or a line of credit that will only be used to manage risk. This helps you safeguard against any cash shortfalls that may occur as a result of a temporary loss of income, renovations that may need to be done, or a reduction in family income.

- Instead of purchasing a high-priced property that will rely heavily on one rental income, consider purchasing two lower-priced properties in different areas to reduce the potential cash flow risks that may occur if you can’t find a tenant for a considerable period.

- Take out income insurance so that you can continue to receive ongoing income in the event that you or another family member suffer a loss of income due to sickness or accident. Income insurance should pay you 75% of your income up until the age of 65 and is 100% tax deductible.

- Take out life insurance to ensure that in the event of death, your investment and family home loans can be paid down to ensure financial security for your surviving beneficiaries.

- Invest only in solid growth assets that have proven track records of reliable income streams and capital growth.

- Invest for the long term to give your investments enough time to grow in value.

- Talk to a qualified tax accountant and financial adviser about the taxation implications, as any benefit from negative gearing will depend on your personal circumstances.

As with any investment decision, gearing should be included within a personalised investment strategy that takes into account your personal risk profile and your individual financial situation.

Who is negative gearing ideally suited for?

Negative gearing is not suitable for everyone. We believe that gearing in general is most appropriate for people who fit the following criteria:

- You have high risk tolerance and can accept investment volatility. That is, investment downs more than ups

- You have a strong, secure cash flow with a surplus income after all living expenses that you can allocate towards the ongoing costs of investments

- You have a higher marginal tax rate – ideally between 34.5% and 49%, including the Medicare Levy

- You have either surplus cash savings or equity in property that can be allocated towards purchasing investment assets

- You have an investment time-frame of 7 years or longer

- You have a super balance of $200,000 or more, either your own or a combined fund with your family members

Speak to a wealth accountant todayMake an appointment >Request a callback >

Time is your most valuable asset when gearing

You could spend your whole life trying to determine the best time to invest. But you’d have to be very lucky to pick out the top or bottom of any market.

Remember, investments grow in value over time.

Just think back ten years, and then ten years before that. You would’ve seen many times when share and property markets hit new highs and lows.

But when you look at the prices of property and shares today, you’ll realise that it didn’t really matter whether you picked out the market highs or lows, because the value of any good investment should grow well over time regardless.

So don’t focus on timing the market. Invest for the long term and use your time wisely, because time’s the one thing you can’t get back.

Advanced negative gearing strategies

Tax Effective Accountants are specialists in tax and wealth management. We’ve been helping clients of all ages, incomes and employment use gearing to grow their wealth with our carefully tailored, proven strategies.

We’ve customised strategies to help our clients:

- Purchase and accumulate multiple property and share portfolios

- Purchase property and shares in their personal names, through trusts, through self-managed super funds, and a combination of the three

- Develop properties

- Build granny flats to produce dual income streams

- Use gearing to grow wealth and rapidly reduce debts

- Use self-managed super funds to reduce home loan debt and increase investment portfolios

- Recycle debt – turn non-tax deductible debts into tax deductible debts

- Transfer commercial properties into self-managed super funds

- And much more

Whilst tax is an important element, we don’t recommend gearing strategies be used to minimise taxes. If there is very little potential to make significant capital gains in an investment, we see no real point in negative gearing.

But when used correctly, negative gearing can be an incredibly powerful tool to build up your wealth and investments.

Sharing is caring

If you’re the caring type, please do us a favour and share this important information with your family and friends. Spread the word on your preferred sharing platform now.

We’d really appreciate it.

Share this article by using the share icons below!

I’m interested in using negative gearing to boost my investments and wealth- what now?

Now that you understand how negative gearing works, and all the advantages and risks associated, you may be considering it as an option. From here, it’s important to get professional advice.

The best weapon you can have is an adviser who can make it effortless for you so that you do close to nothing while your investment sits there, steadily building up your wealth.

But be careful. Many advisers make decisions based entirely on their own set approaches without considering your personal situation. Find the adviser who will come up with a strategy tailored for your financial and personal goals before making a move.

If you don’t have somebody like this yet- then try us out for free, no obligations.

Interested in making an appointment to discuss your options? Contact us today.

We’ve covered the basics for you here. Now let us take you to the next level.

Schedule your free financial heath diagnostic valued at $395 with a Tax Effective accountant who will help you:

- Review your current financial position

- Determine whether negative gearing property or shares is right for you

- Work out an ideal property or share purchase price

- How to use gearing to pay off your debts in a fraction of the time

- Consider advanced negative gearing strategies

- And a lot more

Speak to an adviser with the expertise to cover everything you need. Have someone who really knows your situation working on all aspects of your investment, in one place.

Book an appointment with us in minutes- fill out the form below, book through our site or call us at 1300 399 829.

We’re located in the heart of Sydney CBD. But don’t worry. If you don’t live nearby or just don’t have the time to come in, we service clients Australia-wide through Skype.

E-Book Navigation

Share E-Book with friends