Discover the power of property investing through super

With the high cost of living, together with high debt levels, it can be difficult to allocate as much money as you’d like to growing your family wealth.

The introduction of the 2017 Super Reforms has made it even more difficult, with the new contribution limits restricting how much money you can put into the concessional taxes super environment to help accelerate your wealth.

This means that a majority of Australians will retire with insufficient funds to allow them to live the lifestyle they want when they retire.

Self-managed super funds can be extremely powerful investment tools, and with the right strategies in place, can help you significantly grow your retirement savings.

The purpose of this e-book is to help you understand how you can accelerate your super investment growth by borrowing money to buy property with a self-managed super fund.

This strategy has helped many of our clients grow their net super balance by hundreds of thousands of dollars plus, with little super cash flow risk.

Borrowing money to buy property through super isn’t for everyone.

But if you have at least $200,000 in super or can combine the super balances of up to 4 family members of $200,000, we seriously recommend that you consider an SMSF borrowing strategy.

Next steps, after reading the SMSF property investing e-book

If you’d like more information or want to get in touch with a qualified SMSF accountant or financial planner to discuss property investing through super and how it could work for you, feel free to contact one of our SMSF specialists today.

Speak to a SMSF accountant todayMake an appointmentRequest a callback

Disclaimer

This e-book has been written by Tax Effective Accountants.

The information contained is general information only and does not take into consideration your personal financial situation, goals and obligations.

This e-book should not be used as a substitute for financial advice.

Self-managed super rules can be complex. So, if you are considering borrowing money to buy a property through super, we recommend that you talk to a qualified accountant or financial planner to find out whether an SMSF gearing strategy is appropriate for you.

Tax Effective Accountants assumes no responsibility for any actions you take without seeking professional advice.

Contents

- Introduction to SMSF property investments

- SMSF - Limited Recourse Borrowing Arrangements

- 6 big reasons why you should consider buying property through super

- What are the risks of borrowing to buy property through super

- What properties can and can’t be purchased through your super?

- Understanding implications of repairs and improvements

- Step-by step guide to setting up a LRBA and buying property through super

- Client case study 1

- Client case study 2

- Conclusion on borrowing money to buy property in an SMSF

- Claim your free SMSF consultation with an expert

- Contact

Introduction to SMSF Property Investment

A self-managed super fund (SMSF) is a retirement savings account that can be run by one person or up to four family members who can combine their super balances and invest funds together.

Unlike retail and industry super funds, SMSFs aren’t run by large corporate trustees, fund managers, banks or industry bodies. They’re run by the members of the fund.

Self-managed super funds are regulated by the Australian Taxation Office and have to adhere to special rules and regulations.

As long as the members follow the rules, the fund will enjoy significant taxation concessions. That is:

1. Income earnings on all investments will be taxed at a maximum of 15%

2. If you hold an asset for more than 12 months, capital gains tax will be taxed at a maximum of 10%

Because much less of your money is taken in taxes compared to when you invest in your own name, investment returns are substantially higher in SMSFs - so you can really accelerate long-term growth and multiply the value of your investments.

The beauty of having an SMSF is that you can control what, where and when your super money is invested.

You can also buy direct property with an SMSF, which you can’t with traditional super funds - that includes residential investment and commercial property, which makes them extremely attractive to those who prefer to invest in property rather than shares.

Prior to September 2007, SMSFs weren’t able to borrow money to buy property, so only funds with enough cash to buy property outright had the option of buying property through super.

Speak to a SMSF accountant today Make an appointmentRequest a callback

SMSF - Limited Recourse Borrowing Arrangements

In 2007, the rules changed for the better. The government introduced a borrowing exception. As long as your fund satisfied a set of specific criteria, SMSFs could borrow money to invest in property and shares.

The problem was, the new legislation wasn’t clear and this created a lot of uncertainty and confusion.

So, in 2010, new legislation was passed, providing greater certainty and clarity to the borrowing exception. It also reduced the borrowing risks for SMSF trustees.

This exception is referred to as a Limited Recourse Borrowing Arrangement (LRBA).

There are 4 basic principles to this (LRBA) arrangement.

1. SMSFs can borrow money from a lender, but the loan must be “limited in recourse”

If an SMSF can’t repay, or defaults on a loan, the lender can only seize the asset or property that was purchased with the money it borrowed. They can’t touch any of the other assets in the SMSF, ensuring that you remaining super fund assets are protected.

2. The borrowed money has to be used to purchase a “single acquirable asset”

The borrowed money must be used to acquire a residential or commercial property that meets the definition of a single acquirable asset. We’ll discuss this in the ‘What properties an SMSF can and can’t buy’ section.

3. The property must be held in trust for the SMSF

The property being purchased has to be held in a separate property trust, called a bare trust or security custodian. The bare trust holds the legal ownership of the property, whilst the beneficial interest- or the right to enjoy and receive the benefits- of the property belongs to the superannuation fund and its members.

This is to provide the super fund with an additional layer of asset protection.

4. The SMSF has the right to transfer the asset (property) to the fund once the loan has been repaid

Once the property has been paid down in full, the title (or ownership) of the property held in the bare trust can be transferred from that trust to the self-managed super fund.

6 big reasons why you should consider buying property through super

1. Investment leverage for greater investment returns

Borrowing allows you to buy assets you otherwise couldn’t because your fund doesn’t have enough money to buy them outright.

By borrowing money through super, you can boost the size of your super fund’s investable assets by over 100%. This means your SMSF can achieve higher investment returns and provide you with potentially hundreds of thousands of dollars more to pay for your lifestyle when you start dropping your working days or stop working completely.

Later you’ll see some real-life examples of just how some of our clients have made hundreds of thousands by borrowing money to buy property through their SMSF.

2. Cash flow positive property investing

When you borrow money to buy property through super, your fund has to make a large initial deposit. Unlike when you buy in your own name, where you can put in a deposit as low as 10%, SMSFs are required to put down at least 20-30%.

Because of this, in many cases your super property’s rental income should be greater than your ongoing costs like loan interest repayments, rates, insurance, strata and so on - the ongoing property cash flow is “cash flow positive.”

If the property isn’t cash flow positive, your employer super contributions, together with your property’s rental income, should be more than enough to pay for the ongoing running costs of your property in super.

Again, you can see real-life examples of how this works later on in the e-book.

3. Significant income taxation benefits

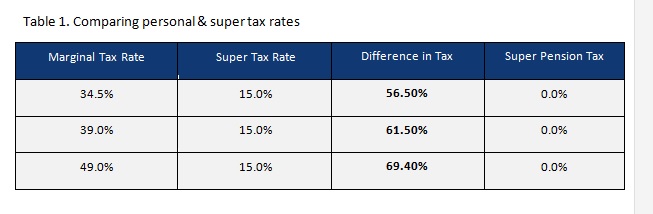

When you purchase property through super, your rental income is taxed at a maximum of 15%. When you compare super taxes to your marginal tax rates, most Australians will pay between 56.5% and 69.4% less tax on rental income through super.

In addition to this, all your ongoing property expenses are 100% tax-deductible to you self- managed super fund, including depreciation allowances that can in reduce and in some cases completely eliminate super investment income and contributions taxes.

And when you retire and convert your super into a pension, SMSF taxes on rental income will drop to zero, so your fund can receive and pay out tax-free rental income to super members.

4. Save potentially hundreds of thousands in capital gains taxes

If you hold your property for 12 months or more in your personal name and then decide to sell, you’ll be entitled to a 50% capital gains tax exemption. This can reduce the tax rate you pay on the capital gains to between 17.25% and 24.5% for most Australians.

However, if the property was held in your super fund, you’d be entitled to a 33% capital gains tax exemption, at the much lower tax rate of 15% - so you’ll only be taxed around 10%.

And if you sold your property when your super’s in the pension phase, your super tax rate should drop to zero.

This can represent a remarkable tax savings of tens or even hundreds of thousands of dollars. This means your super fund would keep a much bigger chunk of the proceeds from selling an investment property than you would if you held it in your own name.

We’ll illustrate by way of example:

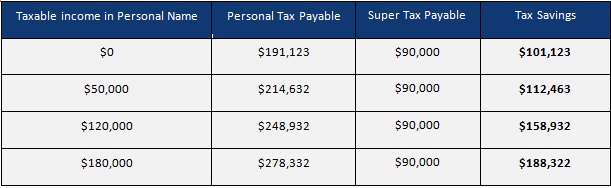

Let’s say you purchased an investment property for $600,000 and the property grew in value to $1,500,000 in 15 years. This is a capital gain of $900,000.

The two tables below illustrate the significant savings in capital gains tax you can achieve when you hold property through super.

Table 2. Capital gains tax calculation on a $900,000 gain in super accumulation phase

This is a risk-free return.As you can see in the above illustration, the amount of money you can keep as a result of paying less capital gains tax if you purchased property in your super can range between $101,123 to $188,322.

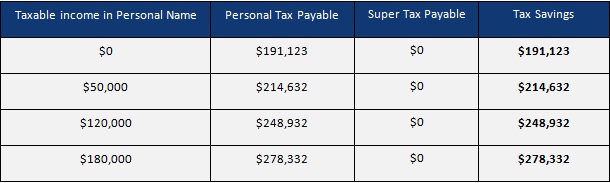

Table 3. Capital gains tax calculation on a $900,000 gain in super pension phase

As illustrated in the table above, the risk-free capital gains tax savings that you would keep if you sell property whilst in pension phase can be more substantial.

That is between $191,123 and $278,332.

5. Rapid debt reduction

Concessional (pre-tax) contributions to your super such as compulsory employer super guarantee, salary sacrifice and personal deductible contributions, can help you pay off your super investment loan in a fraction of the time.

This is because super contributions are taxed at a maximum of 15% rather than at your marginal tax rate. This means that for every dollar you contribute to your loan through super, more money will be available to repay your SMSF loan.

Example

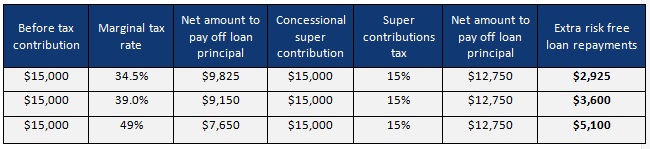

Let’s look at how much more debt can be reduced in super by comparing how much money is left over by someone earning $15,000 in income and using the after-tax proceeds to repay debt versus salary sacrificing $15,000 and using the after contributions tax proceeds to repay debt.

If you had multiple members making concessional contributions, this can significantly reduce both ongoing interest repayments and accelerate debt reduction.As you can see in the above table, the lower taxes taken from super contributions when compared to marginal tax rates provides your super fund between $2,925 and $5,100 more money that can be used to pay off debt.

Note that if the gearing tax benefits reduced the contributions tax within super to zero percent, then the risk-free principal reduction can increase to between $5,175 to $7,350 more.

We’ll illustrate a real example in ‘case study 2’ below.

6. Reduce taxes for high income earners who pay Division 293 taxes

If you earn over $300,000, or over $250,000 as of 1st July 2017, you now have to pay an additional high income contributions tax of 15% on your pre-tax, or concessional super contributions. This can effectively increase your contribution tax by 100% - from 15% to 30%.

Although there are very few ways to reduce your high-income contributions tax, with strategic tax planning through property and share investing, you can reduce the original 15% general concessional contributions tax.

As a result, you can reduce your total concessional contributions taxes to approximately from 30% to 15%.

Hence making super contributions can still be a highly attractive proposition for high-income earners.

Speak to a SMSF accountant today Make an appointmentRequest a callback

What are the risks of borrowing to buy property through super?

So, we’ve looked at the benefits, now let’s look at some of the risks - and how you can manage them.

1. Risk of investment losses

Just like you can magnify returns by gearing into property, you can also make losses in a failing market when you borrow money to buy property through super.

Having said that, when you invest for a longer time horizon, as long as your property is held in a blue-chip location, property prices tend to bounce back pretty quickly.

2. Reduced cash flow due to loss of employment

Where your SMSF property expenses exceed the expected rental income, the shortfall must be met from your concessional contributions.

Whilst in most cases your concessional contributions should be enough to fund this, if you lost your income and no contributions were being made to your super, you might not have enough surplus cash flow available to pay the shortfall.

However, your fund should have enough in cash or liquid assets to maintain any shortfalls for quite some time, until you start working again and contributions start being made into your fund again.

3. Interest rate risk

This is something that should really be considered before you buy a property through super. A sudden increase in interest rates may affect your fund’s cash flow.

We suggest that when you work out the property cash flow that you model your cash flow not on today’s interest rates, but instead make assumptions on a 2% interest rate rise to ensure your super contributions and rental income will be more than enough to fund any shortfall.

If not, you can reduce the amount of money that you borrow by either putting in a larger deposit or purchasing a property at a lower purchase price to reduce the risk.

4. Loss of income due to sickness, accident or death of a member

We went over cash flow problems caused by loss of employment - however, if a loss of income was due to sickness, accident, or death, it could mean that the fund will have to eat into its liquid assets to pay for any property expense shortfall.

Over-time this won’t be sustainable as your liquid asset will begin to deplete.

To minimise this risk, you need to ensure that you have adequate income, life and total and permanent disability insurances in order to minimise or eliminate the impact illness, injury or death of a member will have on your funds cash flow.

What properties can and can’t be purchased through your super?

When borrowing money to buy property through super, it’s important to understand what you can and can’t buy through super, because there are some limitations.

What properties you can buy in an SMSF

A self-managed super fund can purchase:

Houses Townhouses Duplexes Existing and off the plan apartments Office suites Retail shops Other commercial properties Overseas property

What properties can’t you buy in an SMSF

Under the SMSF rules, there are also properties that you cannot buy with an SMSF:

A main residence for yourself Property that you intend to rent out to yourself or related party Property that you or a family member owns - this includes properties owned by trusts and companies that you or another family member controls

You can only purchase a commercial property you or a related party owns, if it’s used only to carry on a business.

Buying properties in an SMSF under Limited Recourse Borrowing Arrangements

Under limited recourse borrowing arrangements, it’s more complicated because the property has to satisfy the “single acquirable asset rule.”

A property is generally classified a single acquirable asset if it’s on a single title or block of land.

But if the property sits on multiple titles it gets a little bit tricky.

For the property to satisfy the single acquirable asset rule with multiple titles:

1. The fixture (the physical property permanently attached to the land) has to be significant to the value of the total asset or land OR

2. Under the State or Territory laws, the titles have to be dealt with together.

It can’t be split into multiple assets- to be a single acquirable asset it must only be considered to be one asset.

As a result, under a limited recourse borrowing arrangement, you cannot buy:

Two or more adjacent blocks of land In most cases, a factory complex on multiple titles An apartment with a car park on a separate title A serviced apartment with furniture package Vacant land that you intend to construct property on separately

It can be extremely difficult to tell whether a property’s a single acquirable asset, and sometimes it may look like it is when it’s not - so it’s important to talk to an expert so that you don’t end up losing a big portion of your money to ATO penalties or failed property settlements.

Before you purchase your SMSF property, speak with an SMSF specialist to ensure that the property being purchases is allowable under super rules - especially when you’re planning on buying through an LRBA.

Speak to a SMSF accountant today Make an appointmentRequest a callback

Understanding implications of repairs and improvements

An SMSF can use borrowed funds under a limited recourse borrowing arrangement to repair or maintain a property held under the LRBA. However, it’s important to understand that borrowed funds can’t be used to improve the property.

Property repairs and maintenance

“Maintaining” refers to work that’s done to a property to prevent defects, damage and deterioration. It ensures that the asset is maintained in its present state.

A “repair” is when you restore or replace a part of an asset that’s damaged or worn out due to wear and tear without changing its character.

A repair is a tax-deductible expense to the fund.

Note that if your SMSF already owns the property, it isn’t possible to use borrowings from a limited recourse borrowing arrangement to repair or maintain it.

Property improvements

“Improving” a property occurs where the functional efficiency or value of the property is substantially increased as a result of adding new features or bringing the asset to a more valuable or desirable condition.

Other factors that point to an improvement include whether the work will increase the property’s ability to produce income and significantly enhance its saleability.

If this has occurred, this would be considered a new replacement or new asset, and thus be forbidden under limited recourse borrowing arrangements.

An improvement is generally classified as a capital expense, so it’s not tax-deductible like property repairs and maintenance.

Determining whether a property repair or improvement has been made can be confusing and mistakes can be made in your interpretation. As a result, we recommend getting an expert opinion to avoid breaching LRBA rules.

How does it all work - Step-by step guide to setting up a LRBA and buying property through super

The set-up of the correct SMSF structure can be quite complicated if you don’t know what you’re doing. We’ve simplified the process into 11 steps for you to get a feel for what’s involved.

Step 1. Seek specialist advice

Because establishing an SMSF with a limited recourse borrowing arrangement (LRBA) is so complex, we recommend that you seek specialist advice.

Work out with a qualified accountant or financial planner:

- How much you have in combined super savings together with any other family member that can join your fund. Remember that you can group your super savings with up to 3 other family members.

- How much each member gets put into super and whether any members plan to make additional salary sacrifice or after-tax contributions

- How much your self-managed super fund can borrow

- Stress test- consider interest rate rises, tenant vacancy and loss of contributions and determine whether your fund could comfortably continue to meet the ongoing SMSF and property expenses

- What is the optimum purchase price for your fund?

After you’ve done this, your SMSF adviser will help you:

- Compare your current super strategy with an SMSF property investment strategy and project how much better off your fund can potentially be over 7 year-plus period

- Understand all the risks associated with gearing

Once you’ve ticked off all these points, you’ll have a good idea of whether buying property through a self-managed super fund is the right super option for you.

If you make the decision to set up an SMSF, a statement of advice will need to be prepared by your accountant or financial adviser prior to setting up the fund.

Step 2. Establish the correct SMSF structure

If you don’t already have an SMSF, you need to establish a fund with a trust deed that allows your self-managed super fund to borrow money to buy a property.

Take care here because not all trust deeds do. We’ve seen cases where people have purchased property through their SMSF and failed to settle because their trust deeds didn’t actually allow it.

If you already have a self-managed super fund, find out whether your existing trust deed allows you to borrow money to buy property. If it doesn’t, you can either amend or change the deed.

The correct SMSF set-up also requires your fund to document its investment strategy.

Step 3. Rollover all member super funds into your self-managed super

In order for your fund to invest or pay for a deposit on an investment property, the funds need to be available in its cash account. All the property costs must come from your super fund - they cannot be paid by you personally and then be paid back to you by your fund.

So, before you start looking, ensure that all member super funds have been rolled over and that all your employer, salary sacrifice, personal deductible and after tax-contributions are flowing through to the SMSF fund’s cash account.

Step 4. Set up a bare trust to hold your SMSF property investment

An SMSF can’t borrow money unless the property is held in what’s called a bare trust, with the SMSF being the beneficiary.

What this means is that the bare trust is the legal owner of the property. They hold the property for the SMSF in trust until the loan is repaid. Once the loan is repaid, investment ownership will be transferred to your SMSF.

So, you’ll need to establish a separate bare trust with a corporate trustee.

The ownership of the property must be in the name of the corporate trustee of the bare trust, not in the name of your SMSF or SMSF trustee.

Step 5. Get your SMSF property loan pre-approved

SMSF loans are different to your traditional bank loans.

Remember, SMSF loans are limited recourse. If you can’t repay your SMSF loan, the bank can only seize the property held in the bare trust. They can’t touch any of your super assets.

This limited recourse borrowing arrangement is designed to protect your SMSF trustee from being personally pursued for the debt generated from the SMSF.

Because of this, lenders typically require a 30% deposit and limit their loans to 70% of the purchase price. Some banks, however, will still allow you to borrow 80%.

As an additional layer of safety, the banks generally require an additional 10% in liquid assets to be held by the SMSF or SMSF members. This means an SMSF should have approximately 30-40% plus costs in their fund to secure an LRBA.

Note that SMSF lenders charge higher interest rates.

Unlike traditional investment loans, SMSF loans don’t come with interest rate discounts that banks provide individual borrowers.

On average, SMSF loans are about 1% higher in interest rates.

Now that your SMSF has a loan pre-approval, this will give you your property price range.

Do your research, crunch the numbers and understand the cash flow. And importantly- take your time.

Important things to consider:

- Demographics: what are the tenant demographics in the area – white collar professionals, tradies, employment rates, income levels

- Jobs: what kind of employment is in or around the area, proximity to CBD

- Transport: How close is the property to train stations, bus stops, light rail<

- Shops: Are you in close proximity to shops and major shopping centres

- Recreation: Are you close to parks, river, beach

- Vacancy rates: Does the suburb have low vacancy rates

- Type of property: Is the property the right fit for the area- for example; a studio apartment in a suburban area with high family ratios may not be the right property for the suburb

Once you’ve found your property, the contract of sale will be sent to your solicitor.

Step 7. Book in a time to see your solicitor

Be very careful when you choose your solicitor or conveyancer. Buying property through a self-managed super fund is a lot more technical than purchasing a property in your individual name.

There are a lot of SMSF rules that your solicitor needs to be familiar with.

We’ve seen a number of cases where the SMSF member’s solicitor didn’t understand the complex rules surrounding limited recourse borrowing arrangements, leading to mistakes that cost the SMSF tens of thousands to fix.

So, make sure your solicitor is experienced with SMSF property transactions.

Once you and your solicitor are happy with the contract, you’ll be required to provide your 10% deposit and exchange contracts.

Step 8. Amend your SMSF property investment loan application

Once you’ve signed and exchanged contracts, go back to your lender and provide them with your contract of sale and rental letter to confirm the proposed rental income the property will pay.

At this stage, you’ll also be required to decide:

The loan term i.e. 25 or 30 years Whether you take out a fixed or variable loan Whether you make principal and interest or interest only loan repayments Whether you establish an offset facility Should you split your loan with a combination of the above?

Once you’ve decided, a valuation will be done by the bank on your property.

After the valuation has been accepted, the loan documents will be issued.

You will then have to make an appointment to go over these with your solicitor again. This is because your solicitor is required to sign a solicitor’s certificate that’s attached to the loan documents.

Once you and your solicitor have signed the loan contract and legal documentation, the executed documents will be sent back to the bank to get certified.

A settlement date will then be determined.

Step 9. Find a good property manager to find you quality tenants

Just because your agent sold you your SMSF property, it doesn’t mean they’re a good property manager. Or maybe they are.

The point is, you need to talk to a number of agents/property managers to find the best deal.

Find out how much rent they think they can achieve and what they charge. Also find out what you get for the fee. An average fee for your property management would sit around 5.5% of the rental income received.

We recommend agents that will simplify the rental process for you and pay all your property expenses out of the rental income they receive.

Once you’re comfortable with an agent, you’ll be required to sign a property management agreement. Your agent will then advertise your property for rent.

Step 10. Settle your SMSF property investment

A day or so before settlement, your solicitor will advise you that you need to provide a cheque from your SMSF to make up the shortfall required to settle the property.

This shortfall amount includes the outstanding 10% or 20% deposit plus stamp duty, loan costs and legal fees.

On the day of settlement your solicitor will organise for all the funds to be paid out, including the loan.

Once this is done, your property will settle - the title will be transferred to the trustee of your bare trust.

The keys will be handed over.

Step 11. Receiving property rental income and paying SMSF property expenses

Though the legal owner of your SMSF property is the trustee of the bare trust, no rental income is paid to the trustee or the bare trust nor are the ongoing property expenses including loan repayments, rates, strata and property management expense paid by the trustee of the bare trust.

The rental income must be paid by your property manager to your SMSF bank account. The rental income cannot be paid to your personal bank account and then transferred to your SMSF.

Likewise, all ongoing property expenses have to be paid out of your SMSF bank account.

Here’s a visual depiction of how it all works

Now that your SMSF has a loan pre-approval, this will give you your property price range.

Do your research, crunch the numbers and understand the cash flow. And importantly- take your time.

Important things to consider:

- Demographics: what are the tenant demographics in the area – white collar professionals, tradies, employment rates, income levels

- Jobs: what kind of employment is in or around the area, proximity to CBD

- Transport: How close is the property to train stations, bus stops, light rail<

- Shops: Are you in close proximity to shops and major shopping centres

- Recreation: Are you close to parks, river, beach

- Vacancy rates: Does the suburb have low vacancy rates

- Type of property: Is the property the right fit for the area- for example; a studio apartment in a suburban area with high family ratios may not be the right property for the suburb

Once you’ve found your property, the contract of sale will be sent to your solicitor.

Step 7. Book in a time to see your solicitor

Be very careful when you choose your solicitor or conveyancer. Buying property through a self-managed super fund is a lot more technical than purchasing a property in your individual name.

There are a lot of SMSF rules that your solicitor needs to be familiar with.

We’ve seen a number of cases where the SMSF member’s solicitor didn’t understand the complex rules surrounding limited recourse borrowing arrangements, leading to mistakes that cost the SMSF tens of thousands to fix.

So, make sure your solicitor is experienced with SMSF property transactions.

Once you and your solicitor are happy with the contract, you’ll be required to provide your 10% deposit and exchange contracts.

Step 8. Amend your SMSF property investment loan application

Once you’ve signed and exchanged contracts, go back to your lender and provide them with your contract of sale and rental letter to confirm the proposed rental income the property will pay.

At this stage, you’ll also be required to decide:

The loan term i.e. 25 or 30 years Whether you take out a fixed or variable loan Whether you make principal and interest or interest only loan repayments Whether you establish an offset facility Should you split your loan with a combination of the above?

Once you’ve decided, a valuation will be done by the bank on your property.

After the valuation has been accepted, the loan documents will be issued.

You will then have to make an appointment to go over these with your solicitor again. This is because your solicitor is required to sign a solicitor’s certificate that’s attached to the loan documents.

Once you and your solicitor have signed the loan contract and legal documentation, the executed documents will be sent back to the bank to get certified.

A settlement date will then be determined.

Step 9. Find a good property manager to find you quality tenants

Just because your agent sold you your SMSF property, it doesn’t mean they’re a good property manager. Or maybe they are.

The point is, you need to talk to a number of agents/property managers to find the best deal.

Find out how much rent they think they can achieve and what they charge. Also find out what you get for the fee. An average fee for your property management would sit around 5.5% of the rental income received.

We recommend agents that will simplify the rental process for you and pay all your property expenses out of the rental income they receive.

Once you’re comfortable with an agent, you’ll be required to sign a property management agreement. Your agent will then advertise your property for rent.

Step 10. Settle your SMSF property investment

A day or so before settlement, your solicitor will advise you that you need to provide a cheque from your SMSF to make up the shortfall required to settle the property.

This shortfall amount includes the outstanding 10% or 20% deposit plus stamp duty, loan costs and legal fees.

On the day of settlement your solicitor will organise for all the funds to be paid out, including the loan.

Once this is done, your property will settle - the title will be transferred to the trustee of your bare trust.

The keys will be handed over.

Step 11. Receiving property rental income and paying SMSF property expenses

Though the legal owner of your SMSF property is the trustee of the bare trust, no rental income is paid to the trustee or the bare trust nor are the ongoing property expenses including loan repayments, rates, strata and property management expense paid by the trustee of the bare trust.

The rental income must be paid by your property manager to your SMSF bank account. The rental income cannot be paid to your personal bank account and then transferred to your SMSF.

Likewise, all ongoing property expenses have to be paid out of your SMSF bank account.

Here’s a visual depiction of how it all works

Speak to an SMSF accountant today Make an appointmentRequest a callback

Client case study 1

How Nancy increased her net after-debt super balance from $126,000 to $528,333 in under 5 years by borrowing to buy property through a self-managed super fund

We met Nancy, aged 50, approximately 4 years ago. She earned $120,000 per annum and had a retail super fund with a balance of $126,000 and no other assets outside her family home. Her employer paid the 9.5% compulsory employer super contributions.

Nancy wanted to retire at the age of 65.

We needed a strategy that could really multiply her retirement savings- so we went over her options and advised her to establish a self-managed super fund and borrow money to buy an investment property through it.

Otherwise, with just her employer super contributions, she wouldn’t be able to grow her super enough to retire when she hoped to.

We helped Nancy determine an appropriate purchase price that she could comfortably afford to cash flow, however, she didn’t have enough money to put down a deposit plus costs to buy anything at that price.

So, we advised her that she can consider buying a property off the plan that would be built in around 2 years. If she salary sacrificed approximately $13,600 per annum into super she would have sufficient funds to complete the purchase, assuming the property market didn’t drop.

Nancy decided on a brand new 2-bedroom unit in Sydney’s inner west at $560,000 in June 2012.

The property was completed and settled in April 2015.

Nancy put in a 20% deposit plus costs ($136,790) and borrowed $448,000 at a fixed interest rate of 5.04%.

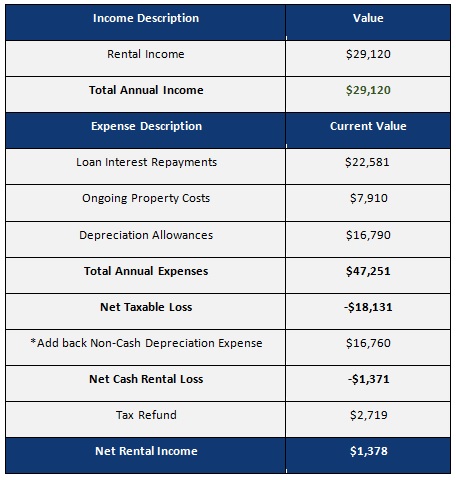

She receives $560 a week in rent and pays ongoing property expenses of $7,910. The property also provides her with another $16,760 in depreciation allowances.

Note that in the 2017 Federal Budget, the government announced that they intend to limit the depreciation deductions property investors can claim.

Under the new rules which are yet to be legislated by Parliament, investors will be able to depreciate new plant and equipment assets within a new property and items they add to their property; however subsequent owners who acquire a property after 9th of May 2017 will not be able to claim depreciation on existing plant and equipment assets.

Investors will still be able to claim qualifying capital works (building costs) deductions, including any additional capital works carried out by themselves or a previous owner.

The budget notes were clear that existing investments will be grandfathered. This means that anyone who has purchased a property up until the 9th of May 2017 will be able to claim depreciation as per normal. The new legislation will be in force from 1st of July 2017.

Hence, the proposed changes to depreciation deductions make buying off-the-plan or brand new property still a very attractive proposition for SMSF property investing.

Net property cash flow can be summarised as follows:

*Non-cash deductions are the depreciation deductions. Depreciation is an expense for tax purposes but not an out of pocket cost, which is the reason it is added back.

As you can see in the table above, Nancy’s property provided her with a $1,378 positive cash flow but is technically negatively geared.

In other words, the property pays for itself.

Strategy outcomes:

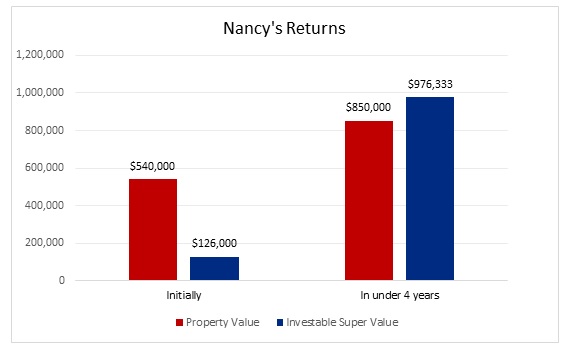

Nancy’s property has grown from $540,000 to $850,000.

This increased her investable super balance from $126,000 when we first met to $976,333 in under 5 years.

If we subtract the $448,000 loan, Nancy has increased her net super balance to $528,333.

This investable amount will continue to compound and achieve accelerated growth every year – not on the net value of $528,333, but on the gross value ($976,333) of Nancy’s super investments, significantly increasing the long-term growth prospects of Nancy’s fund.

Nancy’s property is cash flow positive by $1,378 which means that the property pays for itself and her net employer and salary sacrifice contributions can be used to repay her debt or invest in the share market.

Right now, Nancy is doing a combination of the two. That is using half the funds to reduce her SMSF debt and the other half is invested in the share markets.

Speak to a SMSF accountant today Make an appointmentRequest a callback

Client case study 2

How James and Barbara will pay down their SMSF loan in under 8 years whilst achieving compound growth on a property and share portfolio

We met with James and Barbara in 2016. They’re in their early 50s and earn $180,000 and $96,000 respectively.

They wanted to take control of their retirement savings and find out if borrowing money to buy property through super was a viable option for them. Their aim was to buy a property and pay it off so that they could have a tax-free rental income stream to help them save for retirement.

James wanted to increase his super by making an additional $7,900 per annum in salary sacrifice contributions, and Barbara an additional $15,880.

They had a combined super total of $609,316.

We established an SMSF with the legal structure required to allow it to borrow money to buy property, and rolled over their funds from their existing super.

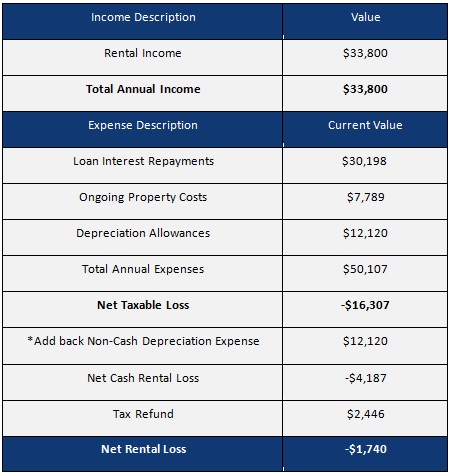

In April 2017, they found a 4-bedroom townhouse valued at $719,000 to purchase in their SMSF with a rental income of $650 per week, ongoing property costs of $7,789 and a loan interest rate of 6%.

They also have a depreciation schedule that states a depreciation allowance of approximately $12,120.

We advised them to limit their initial expenditure to a deposit of 30% plus costs ($246,080) and borrow $503,300. Because reducing debt was important to them, we recommended that they use their surplus super cash flow, after paying all property and fund expenses, to pay down the principal of their SMSF loan.

We also advised that they invest the remainder of their funds (approximately $363,000) in a share portfolio that will provide excellent long term growth that complements their rental income to increase their tax-free retirement pension.

Net property cash flow can be summarised as follows:

*Non-cash deductions are the depreciation deductions. Depreciation is an expense for tax purposes but not an out of pocket cost, which is the reason it is added back.

As, you can see the property is cash flow negative by only $1,741.

However, with $50,000 in yearly super contributions and dividend income, their SMSF can easily pay the $1,741 shortfall and fund fees and still retain a surplus income of approximately $55,066 in the first year.

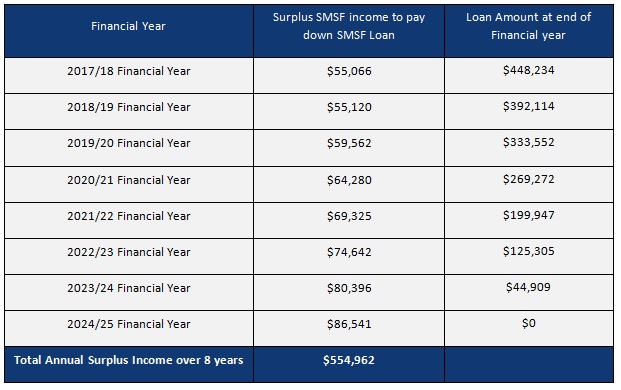

Projected summary of surplus SMSF income to pay down $503,300 original loan

As illustrated above, we estimate that James and Barbara should be able to pay off their SMSF loan of $503,300 in under 8 years.

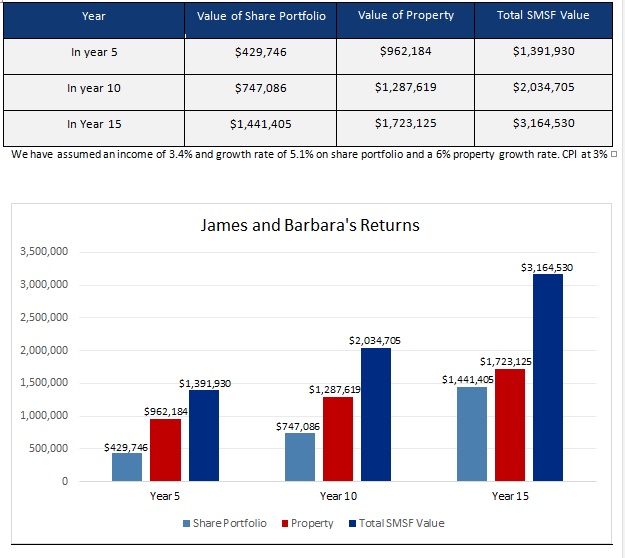

Projected summary of SMSF Growth

Projected strategy outcomes:

By redirecting their surplus SMSF income into their SMSF loan, James and Barbara should be able to pay down their $503,300 loan in under 8 years.

When they retire in 15 years’ time, they should have a tax-free rental income of $51,266 per annum to complement a share portfolio that should pay an additional $66,032 per annum in dividends, bringing the tax free-income they can pay to themselves up to $117,298 per annum.

James and Barbara should also have access to liquid shares valued at $1,441,405 to pay for any lifestyle expenses.

In addition to this, they should also have a property valued at $1,723,125 in 15 years with no debt owing on it.

Their SMSF’s funds should continue to grow in value, even in retirement.

Conclusion on borrowing money to buy property in an SMSF

As you can see, borrowing money to buy property through super can go a long way in building a huge amount of tax-free wealth for when you retire.

However, it’s a complex area and can be a little bit intimidating and tricky.

If you have $200,000 or more in your super or a combined super with up to four family members in it, SMSF borrowing is definitely a strategy we highly recommend that you consider.

This strategy’s suitable for you if your investment time horizon is 7 years plus. We don’t recommend it for horizons shorter than this.

Sharing is caring

Do you have any like-minded family or friends that would appreciate or enjoy reading this e-book on SMSF property investing?

Interested in learning more about SMSF property investing?

Tax Effective Accountants are specialists self-managed super fund accountants and advisers in the Sydney CBD.

We provide an A-Z SMSF solution to individuals, families and business owners all around Australia and have been helping clients achieve remarkable results.

From SMSF set-ups, tax and accounting, to SMSF gearing, portfolio management and investment strategies – we do it all.

Schedule your free super health diagnostic valued at $395 with a Tax Effective SMSF accountant who will help you:

Review your current super position Determine whether SMSF property investing is right for you Work out an ideal SMSF property purchase price Pay off your SMSF property investment loan in a fraction of the time Consider advanced SMSF tax and investment strategies And a lot more

If you don’t live in Sydney or can’t make it to our Sydney CBD office, that’s okay, we service clients all around Australia via SKYPE.

E-Book Navigation

Share E-Book with friends