Unleash the power of your super

David & Tannya were a typical couple who were worried they wouldn’t have enough money to pay out all their debts and live the life they wanted in retirement.

They were right to be concerned, because the path they were on would not have allowed them to build the wealth they needed.

But then David & Tannya visited Tax Effective.

At the time, they had a combined $659,940 in superannuation. Ten years later, they had grown their nest egg to $3,582,422, to set themselves up for an incredible retirement.

So what changed?

The answer is that David & Tannya implemented the advanced SMSF (self-managed superannuation fund) strategies and structures recommended by our experienced SMSF accountants. That allowed them to:

-

Build a self-funding property portfolio valued at $2.32 million

-

Build an exchange-traded fund (ETF) portfolio valued at $761,173

-

Accumulate over $501,249 in their SMSF loan offset account

-

Reduce their SMSF contributions and investment income tax to 0%

-

Accumulate a capital gain of $1,577,054

-

Save hundreds of thousands of dollars in unnecessary capital gains taxes when they sell their investments

You might be wondering: if David & Tannya were just a typical couple, how could they build so much wealth so quickly?

The answer is that SMSFs are powerful investment vehicles with special tax status, including a nil capital gains tax environment when you sell assets in pension phase.

David & Tannya's three big problems

When we first met the couple, David (age 45) was earning a $320,000 salary, while Tannya (43) was earning quite a bit less because she was working part time while completing a university degree. So while their combined household income was strong, it was not extraordinary.

They were also receiving a combined $30,645 in superannuation contributions, which was expected to increase by about $10,000 once Tanya returned to full-time work. At the time, their combined super balance was $659,940.

Sadly, that super balance was not as large as it could’ve been.

That’s because David & Tannya did not have any tax-effective super strategies in place, despite seeing several other (less proactive) accountants over the years.

So they asked Tax Effective to review their super arrangements to discover if they were maximising their investment potential – and, if not, to advise how to do so.

After conducting our review, we discovered David & Tannya had three big problems:

They weren't using any tax minimisation strategies within their super fund

-

And, perhaps most importantly, they had no tax structures in place that could significantly minimise their taxes.

How Tax Effective solved David & Tannya's three big problems

We helped David & Tannya solve all three problems by setting up an SMSF and transferring all their super savings into their new fund. That allowed David & Tannya to:

-

Take full control over their super investments

-

By borrowing through an SMSF, you can significantly increase the investable value of the fund whilst reducing contributions taxes and income taxes – in many cases to zero, as David & Tannya did – thereby increasing your return on investment.

Also, when your super savings are as large as David & Tannya's, it costs less to run an SMSF than use an industry super fund (as they were previously doing).

SMSF Strategy #1 - Use leverage to buy two investment properties

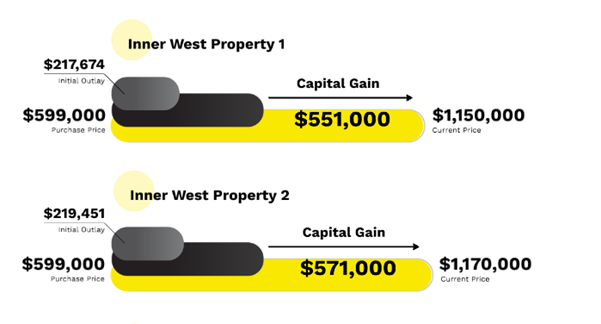

We calculated that David & Tannya could buy two investment properties in the Inner West of Sydney, each valued at $599,000.

So by contributing a combined $436,451, they were able to immediately acquire property assets worth $1.198 million.

-

Property 1 = they put down $217,000 (30% deposit plus costs) and borrowed $419,300

-

While David & Tannya now had $838,600 in loans as well as ongoing property expenses, we knew the money to cover these costs would come from their tenants, employer super contributions and tax savings.

After 10 years, the combined value of their properties had increased from $1.198 million to $2.230 million, for a capital gain of $1.122 million. At no point during that decade did David & Tannya need to make any additional contributions from their personal savings.

This investment strategy also allowed David & Tannya to eliminate their super contributions tax, which meant more of their returns were retained in the fund, giving them a risk-free return on investment.

Strategy #2 - Use leverage to buy a portfolio of Exchange Traded Funds (ETFs)

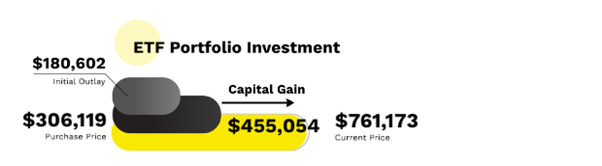

David & Tannya were able to accumulate a good cash surplus in their SMSF during the first two years, so we advised them to diversify their portfolio, to include more than just cash and residential property.

So we used $306,119 (with $180,602 coming from their SMSF savings and $125,517 from borrowings) to buy a portfolio of exchanged-traded funds (ETFs) listed on the Australian Securities Exchange.

As with David & Tannya’s property investments, the cost to fund the ETF portfolio was paid for by their employer super contributions.

After eight years, their ETF portfolio had more than doubled in value, to $761,173, despite some downturns in the stock market over the last six month. So they had accumulated $455,054 in capital gains.

Strategy #3 - Debt reduction and risk minimisation

Real Client Success Stories

Nestor

Medical Professional

We designed a custom plan helping Nestor save $31,500 per annum in taxes, instantly pay off his non-tax deductible home loan debt and eliminating hundreds of thousands of dollars in future capital gains tax liabilities.

Alan and Stephanie

Professional Couple

Alan and Stephanie are executives who were paying tax at the highest marginal tax rate of 47%. So we designed a custom strategy that reduced their taxable income by $48,980 and increased their net wealth by $912,000 in just four years.

Joe

Business Owner

We created a plan to help Joe automate his business while implementing business and personal tax strategies and trust structures that helped him save $123,000 in taxes per annum. Our plan also enabled his expansion into four new profitable businesses while amassing a sizable property investment and share portfolio.

Schedule a no-obligation consultation with an expert SMSF accountant to find out how you could massively increase your super through a self-managed super fund today.